The only card you need

First, how pathetic is it that VISA can’t even come up with an original idea?

If you’re not familiar, American Express created its mythic Centurion card, known to the proletariat as the “black card”, in 1999. Beyond gold, beyond platinum, beyond californium or whatever the most expensive element in the periodic table now is, the Centurion card was available to such an exclusive subset of American Express cardholders that the company barely acknowledged its existence, let alone advertised it. If you qualified, they’d let you know. They’d also charge you $7500 for the privilege, plus a $2500 annual fee. Even today, in a world where the internet has made secrets scarcer and harder to keep, the card retains as discreet a profile as possible. The card’s website, Centurion.com, is not what you’d call ostentatious.

Even though credit cards have evolved and been democratized, turning from status symbols into mere necessities, the American Express brand still manages to retain some kind of cachet. Looking to challenge that cachet, in 2008 VISA introduced its Centurion competitor – the unoriginally monikered Black Card®. Seriously, that’s what they called it. Imagine Honda calling its new economy car the Bug, or the Cincinnati Bengals calling their end zone bleacher section the Dawg Pound, and you’d have an idea how this dances around the edge of copyright infringement without stepping over.

How about some other, more legitimate reasons why the Black Card (capitalized) is absurd? For one thing, it’s Made of Stainless Steel℠. And yes, they really did go to the trouble of attaching a service mark to that phrase. Exactly how is that a plus? So you can impress the clerk with an authoritative clink while slapping your card down on the marble desk at the Mandarin Oriental? Or is it to garner even more attention from TSA agents while shuffling through the shoeless indignity that is modern American air travel? Either way, that sounds like the opposite of the discretion that most truly wealthy people prefer.

You know what our PayPal accounts are made out of? Nothing. Literally, nothing. Neither are our bank’s wire transfers and direct deposits. If only they were made from (excuse us, “forged”–sounds classier) stainless steel, we’d be enjoying a money-having experience far superior to that endured by the huddled middle class.

Here’s what $495 gets you, assuming VISA selects you to buy your way into Black Card membership:

- A magazine. Not just any magazine, but “the ultimate luxury guide [that] showcases the finest in travel, fashion, transportation, technology, interior design and art.” It’s for members only, just like the jackets. Again, we have the internet now. If information exists in printed or printable form, it’s available to everyone. Even entry-level cardholders. Besides, magazines, at least at our house, are literally* garbage. (If you want the latest issue of American Rifleman or Vegas Living, you’re welcome to wade through our trash cans.) These days, a magazine is something you buy at an airport newsstand because you want something to read, your Kindle is low on juice, and you can’t be bothered to fish its power cord out of your luggage and find a place to sit that’s near a power outlet. Speaking of airports,

- Visits at “over 350 lounges in 200 cities worldwide.” Wow, that’s more than 1.75 lounges per city. We’re not here to denigrate airport lounges in principle, as sitting with the masses can sometimes be its own punishment. But if you’re spending so much time waiting for connecting flights that this sounds like an agreeable perk to you, then you’re rich enough that you can find a secretary who can reduce your layovers while she books your flights.

- A 24-hour concierge, who can give you “local shopping information” and details on “highlights/sights/exhibitions/shows.” One more time, the internet. If you can afford $495 for a Black Card, you can afford $495 for an iPhone that will tell you what the time in Incheon, South Korea is without having to call anyone. Besides, if you’re that desperate to live the life of the upwardly-immobile-because-you’re-already-at-the-top, shouldn’t you already have a personal assistant at your beck and call? One who will help you with even more intimate problems than a VISA employee with a headset can? “Hi, Janie? It’s Mr. Smith. What’s the name of that guy we called to bury that hooker last time? No, I don’t need another hooker buried. But he also said he could secure some krokodil, and I was feeling more indulgent than usual tonight. I tried the Black Card concierge and she said she was legally forbidden from helping me with this. Bitch. What am I paying her for?”

And, as if the concierge at a call center in Fort Wayne is going to be able to find you a dog groomer in Madrid any better than you can do it yourself.

- “Global Acceptance. For your convenience, your Black Card is accepted in over 170 countries worldwide with no foreign transaction fees.”

(Just to clarify, that’s for your convenience, and not for your vexation.) Still though, what a perk! It’s not as if every other card with a VISA logo on it isn’t accepted in all those countries.

There’s also a plethora of arcane services that you’re never going to need and certainly wouldn’t be able to justify the $495 purchase of. Like late checkout, which can usually be had by asking the hotel employee nicely. Or “auto rental collision damage waiver,” which you already have if you have car insurance. Or reimbursement for “essential items in the event of baggage delay.” A $3000 laptop doesn’t count as an essential item, either. You get $100 of reimbursement a day up to a total of $300. That’s a lot of dental floss.

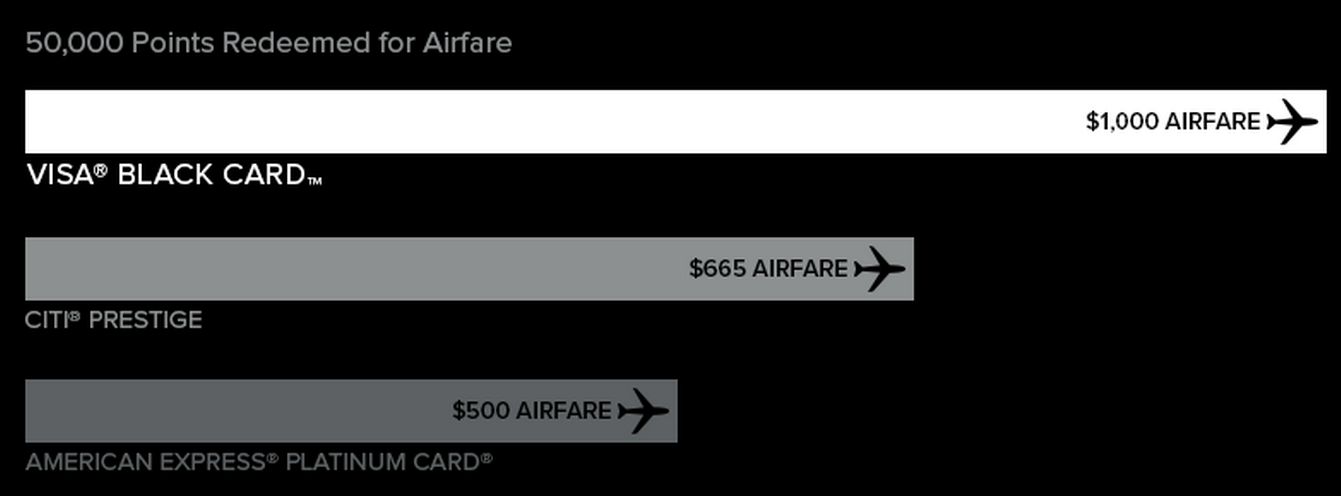

Adorably, VISA compares its own shiny apple to a decomposing American Express orange and doesn’t expect people to notice the unfair comparison:

If the folks at VISA didn’t hate us before–after all, they’ve been losing money on us since we first signed up and started our uninterrupted pattern of paying our balances in full every month, as responsible people do–they probably do now. Glad to be of help.

*That’s 2 uses of “literally” in this post, both of them accurate and neither of them superfluous.