Putting your eggs in multiple baskets is the surest way to minimize risk and build wealth, right? You can add that to the list of homespun nonsense that sounds good but is patently false:

- Wear a stupid wool hat, you lose 60% of your body heat through your head

- The more you shave a particular body part, the faster the hair grows back

- Standing in front of a microwave oven will bombard you with deadly gamma rays

- Smoking is bad for you.

Behold the ETF (exchange-traded fund if you’re new here), a mutual fund that trades on a stock exchange. Like a mutual fund, it consists of the stocks of various companies, often numbering in the hundreds or even thousands. Unlike with a mutual fund, investors can buy and sell ETFs throughout the day. They have a ticker symbol and an immediately available price and everything. Mutual funds’ values aren’t calculated until the day closes and all their components’ prices have settled. Plus mutual funds don’t trade on exchanges, of course.

So what’s a good ETF to invest in? Let’s look atop the leaderboard. Never forget the 1st rule of investing, Past performance is a perfect predictor of future performance.

(Kidding. The line about smoking was deathly serious, though.)

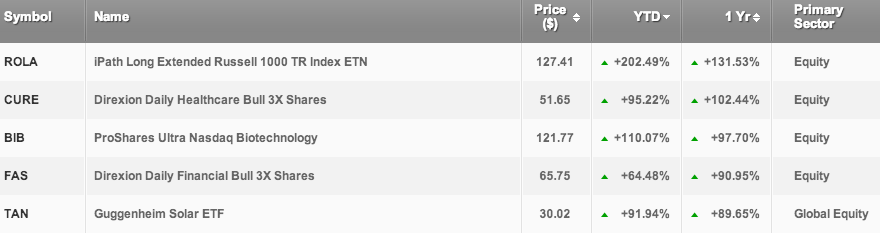

Your top 5 over the past year, regardless of market sector:

Confused? Don’t be. The naming convention is standard: fund company, followed by description. Price is self-explanatory. That’s followed by performance since January 1 and performance since September 18 of last year.

Let’s take a look at the first one, iPath Long Extended Russell 1000 TR Index ETN. iPath isn’t a company, but rather a subsidiary of BlackRock. As for BlackRock, that’s an investment firm with a good reason for concealing its name. It’s owned by public charity case Bank of America, rate-fixing British bank Barclays, and PNC Financial Services (Pittsburgh National Corporation, the eponym of the Pirates’ ballpark.)

The ETF in question is actually an ETN, or exchange-traded note. The difference is that it’s composed of unsecured corporate notes, rather than stocks.

Extended Russell 1000 TR Index means that the ETN tracks the Russell 1000 Total Return Index. That’s an index composed of the prices of 1000 large firms that, according to Russell Investments, represent 92% of the U.S. market. As for Russell Investments, it’s a subsidiary of Northwestern Mutual, an insurance and financial services firm out of Milwaukee. And we are now 3 degrees removed from the subject at hand.

What about the worst fund in existence, defined as the one that’s lost the most money in the past year?

Behold NUGT, the too-clever stock symbol for the Direxion Daily Gold Miners Bull 3X Shares ETF. That’s a name with enough qualifiers that we should deconstruct it:

Direxion. Investment firm founded in 1997, based in Milwaukee. Or as their impregnable website copy puts it,

We offer practical investment solutions to today’s market challenges with a broad suite of highly liquid, institutional-style alternative investment strategies.

Well, that said nothing. What they mean is that the funds they sell are supposed to complement your investments, not be them.

“Institutional-style.” Here are some more empty buzzwords, all from a single “About” page:

- risk-adjusted performance through evolving market conditions

- position portfolios opportunistically for near- and long-term market trends

- access to strategies that provide exposure to multidirectional opportunities

- innovative investment products and services

Innovative? Don’t flatter yourself, Jim. The last “innovative investment product” was the hedge fund. You’re not creating the cotton gin or the mp3 player here.

No wonder most of our recent college graduates can’t find jobs. They can barely communicate.

Daily, in this instance, means that the fund sets daily goals for itself. That alone should be a clue for an individual investor to step back and be cautious. You’re in this for decades, remember? Who gives a damn what an ETF does from Tuesday to Wednesday? We’ll skip over the next couple of qualifiers, get back to them in a minute.

3x. The aforementioned daily goal is to outperform a particular index, and do so threefold. In other words, if the index rises 1% in a given day, the Direxion Daily Gold Miners Bull 3X Shares ETF should rise 3%.

Gold Miners. The index in question is not the Dow, nor even the S&P 500, but something considerably more specialized: the NYSE Arca Gold Miners index.

Do we need to break this down even more? We probably do. The New York Stock Exchange’s most famous index is, of course, the Dow Jones Industrial Average. But that’s just one among hundreds that the NYSE calculates. (Arca, by the way, is short for Archipelago Exchange – a Chicago-based electronic exchange that the NYSE’s parent company bought in 2005. We have to specify “electronic” because unlike NASDAQ and just about every other stock exchange on Earth, the NYSE still, incredibly, conducts much of its business via open outcry. That is, ill-tailored traders yelling at each other.)

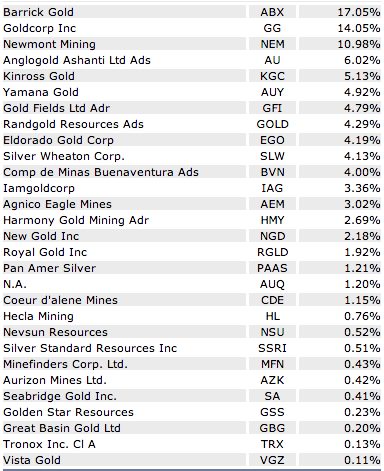

The NYSE Gold Miners index is a constant multiplied by the total of the prices of the stocks of 29 gold mining companies, as follows:

As you can see, the index isn’t close to evenly weighted. By the time you reach the bottom, the companies are small. Golden Star Resources, whose operations consist entirely of 2 mines in Ghana, has a market capitalization of about $140 million. That’s still one more mine than Nevsun has (in Eritrea.) Anyhow, the Gold Miners index changes daily and Direxion tries to beat the changes with this particular ETF.

Finally, Bull. Because there’s a corresponding Bear ETF that tries to do the exact inverse: achieve a daily return 3 times the opposite of the change in the Gold Miners index.

So there you go, with a definition that necessitated a long discussion. Now, onto the question that 99% of ETF owners never bother to ask:

What’s in my fund?

Well, that depends. Seeing as NUGT tries to take advantage of daily price fluctuations, its holdings change every day. Direxion’s own website offers no help on this issue, listing a useless summary of price movements in lieu of a comprehensive list of holdings. This is 2013, we’re better than this.

The good news is that Direxion won’t let you buy its daily funds unless you’ve proven that you’re rich and experienced. But this isn’t just an academic exercise. You owe it to yourself, almost literally, to find out what’s in your mutual funds. We’re teaching you to fish here. It takes just a minute or two. For instance, the T. Rowe Price Value Fund is the most widely held in the world. Regular investors just like you own pieces of it. Google the name of the fund, find its relevant page on the investment firm’s website, find out what it’s composed of, and stop complaining.